The Platform Paradox: Analyzing Activision Blizzard’s Revenue Streams Amidst the Microsoft Acquisition

Introduction: The $68.7 Billion Question

In the high-stakes arena of global technology and entertainment, few events have commanded as much scrutiny as Microsoft’s proposed $68.7 billion acquisition of Activision Blizzard. While headlines often focus on the cultural juggernaut that is Call of Duty or the nostalgic pull of World of Warcraft, a deeper dive into the financial plumbing of the company reveals a startling reality about where the money actually comes from.

A recent analysis of Activision Blizzard’s annual reports, highlighted by industry veteran Nicholas Lovell of Gamesbrief and Hiro Capital, has brought to light a "platform paradox." Despite being the target of a massive acquisition by Microsoft, Activision Blizzard’s revenue dependency on the Xbox platform is surprisingly minimal—accounting for less than 10% of its total intake. This revelation reframes the entire narrative of the acquisition, shifting the focus from console exclusivity to a broader battle for mobile dominance and cross-platform ecosystem control.

Main Facts: A Revenue Breakdown That Defies Expectations

The core of the current industry discourse stems from the 2021 and 2022 financial disclosures provided by Activision Blizzard. To the casual observer, Activision is a "console" company. However, the data suggests it is increasingly a mobile and multi-platform service provider.

The Minority Stake of Microsoft

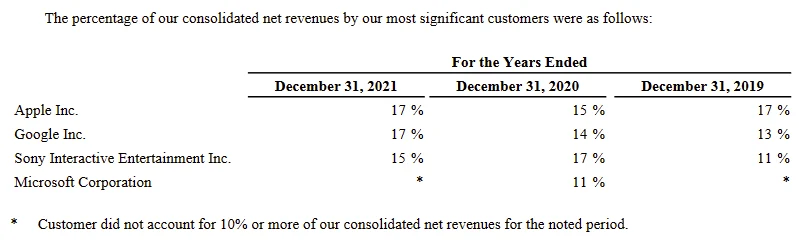

Perhaps the most striking figure is that Microsoft—the very entity seeking to own the publisher—contributes less than 10% of Activision Blizzard’s annual revenue. In the fiscal year leading up to the acquisition announcement, this placed Microsoft behind almost every other major platform partner. For a company valued at nearly $70 billion, the fact that its soon-to-be parent company represents such a small slice of its current earnings suggests that Microsoft is buying for future potential and strategic positioning rather than current cash flow from its own ecosystem.

The Dominance of Sony and Mobile

In contrast to Microsoft’s sub-10% share, Sony’s PlayStation platform consistently accounts for a significantly higher portion of revenue, often cited in the mid-teens (approximately 15-16%). Even more dominant are the mobile titans: Apple and Google. Together, the two main mobile platforms represent roughly one-third (33%) of Activision Blizzard’s total revenue. This is largely driven by King (the makers of Candy Crush) and the successful mobile ports of Call of Duty and Diablo.

The "Missing" 43%

Beyond the big four (Apple, Google, Sony, and Microsoft), approximately 43% of the company’s revenue comes from "elsewhere." This diversified bucket includes:

- Nintendo: Though a major player, Nintendo represents less than 10% of revenue (as it is not individually listed as a major risk factor in SEC filings).

- PC Distribution: Revenue from Steam and Activision’s proprietary Battle.net launcher.

- Direct-to-Consumer: Subscription fees from World of Warcraft.

- Regional Partnerships: Licensing deals in territories like China (notably via NetEase at the time).

- Advertising: In-game advertising revenue, particularly within the King portfolio.

Chronology: The Road to the Largest Deal in Gaming History

To understand how Activision Blizzard reached this revenue distribution, one must look at the strategic pivots made over the last decade.

2016: The King Acquisition

The most significant turning point was the $5.9 billion acquisition of King Digital Entertainment in 2016. This move was initially met with skepticism by "hardcore" gamers but has since proven to be the company’s most consistent engine of growth. It transformed Activision Blizzard from a company dependent on biennial retail hits into a "live service" powerhouse with daily recurring revenue.

2019–2021: The Mobile Pivot

Following the success of King, Activision Blizzard aggressively expanded its internal brands onto mobile. The launch of Call of Duty: Mobile in late 2019 was a watershed moment, proving that AAA console franchises could generate billions on handheld devices. By 2021, mobile revenue had begun to rival console revenue, fundamentally altering the company’s risk profile and platform priorities.

January 2022: The Microsoft Bombshell

Microsoft announced its intent to acquire Activision Blizzard for $95.00 per share in an all-cash transaction. The move was framed by Microsoft CEO Satya Nadella as a play for the "metaverse" and mobile gaming. However, the lopsided revenue data—showing Activision’s reliance on Microsoft’s rivals—immediately set off alarm bells for regulators.

Mid-2022: Regulatory Scrutiny Intensifies

By August 2022, the Federal Trade Commission (FTC) in the United States, the Competition and Markets Authority (CMA) in the UK, and the European Commission began deep-dive investigations. The focus was not just on whether Microsoft would pull Call of Duty from PlayStation, but how the merger would affect the nascent cloud gaming market and the broader distribution of digital content.

Supporting Data: The Financial Weight of the Platforms

The following data points illustrate why the revenue distribution is causing such a stir among analysts and regulators:

| Platform / Source | Estimated Revenue Share | Strategic Significance |

|---|---|---|

| Mobile (Apple/Google) | ~33% | The primary growth engine; high-margin microtransactions. |

| Sony (PlayStation) | ~15-16% | The largest single console partner; vital for Call of Duty. |

| Microsoft (Xbox) | <10% | The "underperformer" in the current portfolio. |

| PC / Other | ~40-43% | Includes Battle.net, Steam, and Nintendo; provides platform independence. |

The "Lina Khan" Factor

The FTC’s review, led by Chair Lina Khan, represents a shift in antitrust philosophy. Historically, regulators focused on the "Consumer Welfare Standard"—essentially asking, "Will this deal lead to higher prices for consumers?"

Under Khan, the FTC has adopted a wider lens, looking at "Vertical Integration" and "Market Foreclosure." The concern here is not that Microsoft will raise the price of games, but that it will use its control over the Windows OS, Azure Cloud, and Xbox hardware to disadvantage rivals. The fact that Microsoft currently represents less than 10% of Activision’s revenue is being used by both sides of the argument:

- Microsoft’s Argument: "We are a small player in the publishing space; we need this deal to compete with the dominance of Sony and mobile giants."

- Regulators’ Concern: "Microsoft is buying its way into a dominant position by acquiring a company that currently thrives on rival platforms."

Official Responses and Strategic Positioning

The stakeholders involved have maintained distinct narratives throughout this process.

Microsoft’s Defense

Microsoft has consistently downplayed its own market power. In various filings, the company has argued that it is "third place" in the console war behind Sony and Nintendo. By highlighting that they account for less than 10% of Activision’s revenue, Microsoft legal teams argue that the acquisition is "pro-competitive" because it allows them to build a more robust mobile presence to challenge the Apple/Google duopoly.

Sony’s Opposition

Sony, unsurprisingly, has been the most vocal critic. Jim Ryan, CEO of Sony Interactive Entertainment, argued that Call of Duty is a "must-have" title that influences console choice. From Sony’s perspective, even if Microsoft currently only accounts for 10% of revenue, the ability to withhold content from the 15-16% of revenue generated on PlayStation gives Microsoft "unprecedented leverage" over the gaming ecosystem.

Activision Blizzard’s Stance

Bobby Kotick, CEO of Activision Blizzard, has framed the deal as a necessity for the company to compete in a world where "tech giants with unlimited resources" (referring to Tencent, NetEase, and Apple) are taking over. The company’s leadership argues that being part of Microsoft provides the capital and infrastructure needed to transition fully into a cloud-based, mobile-first future.

Implications: The Future of the Gaming Landscape

The revenue data provided by Lovell and the annual reports suggests several long-term implications for the industry.

1. The De-prioritization of the Console

If only one-third of a giant like Activision Blizzard’s revenue comes from consoles (Sony and Microsoft combined), the industry is officially in a "post-console" era. The strategic value of the Xbox or PlayStation hardware is becoming secondary to the value of the "Live Service" ecosystem. Microsoft isn’t buying Activision to sell more Xbox consoles; it is buying them to populate its Game Pass subscription service across every screen—PC, mobile, and smart TVs.

2. The "Mobile-First" Mandate

The fact that Apple and Google generate triple the revenue for Activision compared to Microsoft explains the logic of the deal. Microsoft has failed to establish a meaningful mobile presence (the Windows Phone being a historical footnote). By acquiring King and Activision’s mobile divisions, Microsoft instantly becomes one of the largest mobile publishers in the world, bypassing years of failed internal development.

3. The Protection of Sony’s Revenue

As Nicholas Lovell noted, the FTC’s intervention is likely to ensure that Activision’s revenue from Sony remains protected. Regulators will likely demand "behavioral remedies"—legally binding agreements that Microsoft must keep Call of Duty and other major franchises on PlayStation for at least a decade. This creates a strange status quo where Microsoft will technically be one of Sony’s largest and most important developers.

4. The Power of Direct-to-Consumer (D2C)

The 43% of "other" revenue highlights the importance of owning the distribution channel. Blizzard’s Battle.net is a massive asset. By selling directly to players, Activision avoids the "30% platform tax" charged by Apple, Google, and Sony. For Microsoft, integrating Battle.net into the Xbox PC app is a key step in building a unified storefront that can rival Steam.

Conclusion: A Tectonic Shift in Strategy

The revelation that Microsoft accounts for less than 10% of Activision Blizzard’s revenue is a sobering reminder of the current power dynamics in the tech world. It illustrates that the "Console Wars" of the 1990s and 2000s have been replaced by a much larger battle for the "Digital Living Room" and the "Mobile Pocket."

Microsoft’s $68.7 billion bid is an admission that its own platform was not big enough to sustain the future of gaming. By acquiring a company that thrives on the platforms of its rivals, Microsoft is attempting a pivot of historic proportions. Whether regulators allow this "Platform Paradox" to resolve through a merger remains to be seen, but the data makes one thing clear: the future of gaming is mobile, it is cloud-based, and it is no longer confined to the box under your television.