The Strategic Paradox: Analyzing Activision Blizzard’s Revenue Streams Amidst the Microsoft Acquisition

By [Your Publication Name] Staff

The landscape of the global video game industry is undergoing a seismic shift, driven not only by massive consolidation but by a fundamental reorganization of where the money actually comes from. In August 2022, as the Federal Trade Commission (FTC) and global regulators intensified their scrutiny of Microsoft’s proposed $68.7 billion acquisition of Activision Blizzard, a startling revelation emerged from the publisher’s own financial disclosures.

While Microsoft is positioned as the primary suitor for the Call of Duty maker, internal revenue charts reveal a surprising reality: Microsoft accounts for less than 10% of Activision Blizzard’s total revenue. This data point challenges long-held assumptions about the "Big Three" console manufacturers and sheds light on why the mobile sector and rival platforms like Sony’s PlayStation remain the lifeblood of the industry’s biggest third-party publishers.

Main Facts: The Revenue Disparity

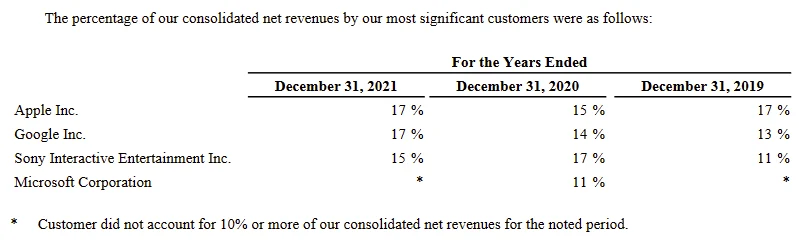

The financial breakdown of Activision Blizzard’s revenue by platform offers a masterclass in the modern gaming economy. According to the company’s 2021 and 2020 annual reports, the distribution of income is far more diversified than the "console wars" narrative suggests.

The most striking figure is Microsoft’s contribution. Despite being the entity attempting to purchase the company, Microsoft (via Xbox and related services) accounted for less than 10% of Activision Blizzard’s annual revenue in 2021. In contrast, Sony—Microsoft’s fiercest competitor in the hardware space—accounted for more than 10%, highlighting a significant reliance on the PlayStation ecosystem for Activision’s console earnings.

Perhaps even more telling is the dominance of mobile platforms. Apple and Google, through their respective app stores, combined to represent approximately one-third (33%) of Activision Blizzard’s total revenue. This is largely driven by the massive success of King (the developer of Candy Crush) and the mobile iterations of Call of Duty.

Furthermore, a substantial 43% of revenue originates from "elsewhere." This "elsewhere" category is a powerhouse of diverse income streams, including:

- Nintendo: Though a major player, Nintendo represents less than 10% of Activision Blizzard’s revenue (as it falls below the SEC’s mandatory disclosure threshold for individual customers).

- PC Platforms: Including Valve’s Steam and Blizzard’s proprietary Battle.net.

- Direct-to-Consumer: Subscription revenue from World of Warcraft and in-game purchases in Overwatch and Hearthstone.

- Regional Platforms: Major distribution hubs in territories like China (via partnerships with NetEase at the time).

- Advertising: A growing segment within the mobile gaming division.

Chronology: The Road to the $68.7 Billion Bid

To understand the weight of these revenue figures, one must look at the timeline of the Microsoft-Activision Blizzard merger, which has become the most scrutinized deal in tech history.

- January 18, 2022: Microsoft shocks the tech and gaming world by announcing its intent to acquire Activision Blizzard for $95.00 per share in an all-cash transaction valued at $68.7 billion. This would make Microsoft the world’s third-largest gaming company by revenue, behind Tencent and Sony.

- Spring 2022: The deal enters the "Phase 1" review process across multiple jurisdictions, including the US, UK, and EU. Concerns immediately arise regarding the exclusivity of "must-have" titles like Call of Duty.

- July 2022: The UK’s Competition and Markets Authority (CMA) signals a deeper investigation, citing potential harm to competition in the console and cloud gaming markets.

- August 2022: Financial analysts and industry experts, including Nicholas Lovell of Gamesbrief, begin dissecting Activision Blizzard’s annual reports. The revelation that Microsoft contributes less than 10% of the target company’s revenue adds a new layer to the antitrust debate.

- Late August 2022: The FTC, led by Chair Lina Khan, adopts a more aggressive stance toward vertical mergers, moving beyond the traditional "consumer price" metric to look at broader ecosystem impacts.

Supporting Data: A Deep Dive into the Numbers

The shift from a console-centric industry to a multi-platform, "live-service" model is reflected clearly in the data. When aggregating the "Big Four" platforms (Apple, Google, Sony, and Microsoft), they accounted for 57% of Activision Blizzard’s revenue in 2020.

The Mobile Juggernaut

The fact that Apple and Google generate more revenue for Activision Blizzard than Sony and Microsoft combined is a testament to the "King" acquisition of 2016. While Call of Duty on consoles captures the headlines, Candy Crush Saga provides the consistent, high-margin cash flow that sustains the business. This explains Microsoft’s strategic interest: the acquisition isn’t just about Xbox; it is a desperate play for a foothold in the mobile market, where Microsoft currently has almost no presence.

The Sony Factor

Sony’s revenue contribution being higher than Microsoft’s (estimated at roughly 15% vs. Microsoft’s <10%) explains why the Japanese giant has been the most vocal opponent of the deal. For Sony, Call of Duty is not just a game; it is a massive revenue generator via the 30% cut Sony takes from digital sales and microtransactions on the PlayStation Store. If Microsoft were to make the franchise exclusive, it wouldn’t just hurt PlayStation’s hardware appeal—it would carve a massive hole in Sony’s annual balance sheet.

The "Missing" 43%

The high percentage of revenue coming from PC and direct-to-consumer channels (43%) highlights the strength of the Blizzard side of the house. Unlike the Activision side, which leans heavily on consoles, Blizzard has a legacy of PC dominance. This "Battle.net" ecosystem allows the company to bypass the 30% "platform tax" charged by console makers and mobile stores, making those revenue dollars significantly more profitable.

Official Responses and Regulatory Stance

The disparity in revenue has fueled different narratives from the involved parties and regulators.

Microsoft’s Perspective

Microsoft has used these figures to argue that it is a "distal third" in the console race. By highlighting that it represents such a small slice of Activision’s revenue, Microsoft’s legal team argues that the company lacks the market power to act as a gatekeeper. Phil Spencer, CEO of Microsoft Gaming, has repeatedly stated that the goal is to "expand access" to games, specifically pointing to mobile and cloud gaming as the primary drivers for the deal.

Sony’s Counter-Argument

Sony Interactive Entertainment, led by Jim Ryan, has dismissed Microsoft’s "underdog" narrative. Sony’s filings to regulators suggest that the 10% figure is irrelevant compared to the "strategic importance" of the IP. Sony argues that even if Microsoft only accounts for a small portion of revenue now, owning the content would allow them to manipulate the market, drive users toward the Game Pass subscription model, and starve the PlayStation ecosystem of its most engaged players.

The FTC and the "Khan Doctrine"

Under the leadership of Lina Khan, the FTC has signaled a shift in antitrust enforcement. Traditionally, regulators focused on whether a merger would lead to higher prices for consumers. However, the FTC is now looking at "vertical foreclosure"—the idea that a company could use its control over a key input (like Call of Duty) to disadvantage rivals in adjacent markets (like cloud gaming or subscription services). The fact that Microsoft currently accounts for so little of Activision’s revenue is, in the eyes of some regulators, evidence of how much room they have to disrupt the existing competitive balance.

Implications for the Industry

The revelation of Activision Blizzard’s revenue structure has several long-term implications for the gaming sector.

1. The Devaluation of Hardware

The data suggests that "platforms" are no longer defined solely by the box under the TV. If consoles (excluding PC) only represent about one-third of the revenue for one of the world’s largest publishers, the "Console War" is effectively over, replaced by an "Ecosystem War." Microsoft’s acquisition is an admission that the Xbox hardware alone is not enough to compete with the reach of mobile devices and the legacy of PC gaming.

2. Vertical Integration as a Necessity

For publishers, the 43% of revenue coming from direct-to-consumer and PC channels is the "holy grail." By owning Activision Blizzard, Microsoft isn’t just buying games; it is buying a direct relationship with hundreds of millions of players, bypassing the fees it would otherwise pay to Apple or Google.

3. The Future of Third-Party Publishing

If this deal closes, it may signal the end of the era of the "independent mega-publisher." If a company as diversified as Activision Blizzard—which earns 90% of its money from platforms other than Microsoft—feels the need to sell to a platform holder, it suggests that the costs and risks of modern AAA game development are becoming unsustainable without the safety net of a trillion-dollar parent company.

4. Regulatory Precedent

The FTC’s wider definition of antitrust harm will be tested here. If the deal is blocked despite Microsoft’s relatively small current share of Activision’s revenue, it will set a precedent that "potential future dominance" is a valid reason to halt a merger. This could chill M&A activity across the entire tech sector.

In conclusion, the financial charts of Activision Blizzard reveal a company that is much more than an "Xbox partner." It is a mobile and PC powerhouse that just happens to sell a lot of copies on PlayStation. As Microsoft seeks to bring that 10% figure up to 100% ownership, the industry watches to see if regulators will prioritize the current diversified reality or the potential for a consolidated future. Nicholas Lovell’s observation remains poignant: "Sometimes, the platforms that we think are big… are not as big as we think." In the case of Xbox and Activision, the smallness of the current footprint is exactly what makes the giant leap of the acquisition so controversial.

Leave a Comment