The Revenue Paradox: Analyzing Activision Blizzard’s Financial Ecosystem Amidst Microsoft’s Acquisition Bid

Executive Summary: The Hidden Reality of Gaming’s Biggest Deal

In the high-stakes world of corporate mergers and acquisitions, few deals have invited as much scrutiny as Microsoft’s proposed $68.7 billion acquisition of Activision Blizzard. While the public discourse often centers on the "Console Wars" and the fate of the Call of Duty franchise, an analysis of Activision Blizzard’s 2020-2021 annual reports reveals a financial landscape that contradicts common industry perceptions.

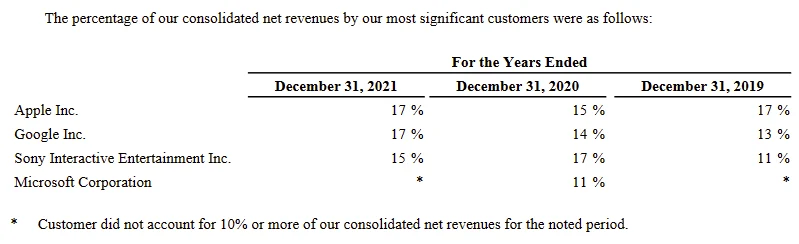

The core of the surprise lies in the revenue distribution across platforms. Despite being the manufacturer of the Xbox, Microsoft accounted for less than 10% of Activision Blizzard’s total revenue prior to the acquisition announcement. In contrast, Sony’s PlayStation—Microsoft’s primary rival—contributed a significantly larger share. Even more striking is the dominance of mobile platforms, with Apple and Google collectively representing approximately one-third of the company’s total intake.

This data suggests that Microsoft’s acquisition is not merely a move to bolster its console lineup, but a strategic pivot toward mobile dominance and a play to capture a diversified revenue stream that currently flows toward its competitors.

Main Facts: Deconstructing the Revenue Streams

To understand the strategic gravity of the Microsoft-Activision deal, one must look at the hard percentages that define Activision Blizzard’s business model. According to the company’s financial disclosures, the traditional console market—long thought to be the heart of the company—is no longer the undisputed king.

The Platform Breakdown

The revenue data paints a picture of a company that has successfully decoupled itself from the dominance of any single hardware manufacturer:

- The Mobile Giants: Apple and Google now represent the largest combined platform share for Activision Blizzard, accounting for roughly 33% of total revenue. This is largely driven by King (the makers of Candy Crush) and the massive success of Call of Duty: Mobile.

- Sony (PlayStation): Sony consistently outpaces Microsoft in terms of revenue contribution to Activision Blizzard. In 2020 and 2021, Sony’s share exceeded the 10% reporting threshold, making it a "major customer" in financial terms.

- Microsoft (Xbox): Perhaps the most startling revelation is that Microsoft accounted for less than 10% of Activision Blizzard’s revenue. This indicates that, as an independent entity, Activision Blizzard was far more dependent on its rivals’ ecosystems than on the ecosystem of its prospective buyer.

- The "Others" (43%): A massive portion of revenue—nearly 43%—comes from sources outside the big four (Apple, Google, Sony, Microsoft). This includes Nintendo, PC platforms like Steam, advertising revenue, and Blizzard’s direct-to-consumer services.

Chronology: From Independent Giant to Acquisition Target

The journey to the current regulatory impasse began years before the 2022 acquisition announcement, rooted in the shifting sands of how games are consumed.

2016–2019: The Pivot to Mobile and Services

During this period, Activision Blizzard intensified its focus on recurring revenue. The acquisition of King in 2016 for $5.9 billion began to pay dividends, shifting the company’s center of gravity toward mobile. Simultaneously, Blizzard moved toward a "live service" model for titles like Overwatch and Hearthstone, reducing the reliance on one-time retail sales.

2020–2021: The Pandemic Boom and Platform Diversification

The COVID-19 pandemic saw a massive surge in gaming engagement. However, the 2020 annual report highlighted a significant trend: the "Big Four" platforms (Apple, Google, Sony, Microsoft) represented 57% of total revenue. This left a substantial 43% of revenue coming from "elsewhere," including the robust PC market and the Nintendo Switch. This era solidified Activision Blizzard as a platform-agnostic powerhouse.

January 2022: The Bombshell Announcement

Microsoft announced its intent to acquire Activision Blizzard for $95.00 per share in an all-cash transaction. The deal was immediately framed by Microsoft as a "mobile-first" strategy, citing the need to compete with Tencent and NetEase.

August 2022: Regulatory Scrutiny Intensifies

By August 2022, the Federal Trade Commission (FTC) in the United States, alongside the UK’s Competition and Markets Authority (CMA) and the European Commission, began deep-dive investigations. This is the period where analysts, including Nicholas Lovell of Gamesbrief, began highlighting the discrepancy between Microsoft’s current revenue share and the potential power shift the acquisition would cause.

Supporting Data: The 43% "Elsewhere" and the Mobile Surge

The "elsewhere" category, which accounts for 43% of Activision Blizzard’s revenue, is the most complex part of the company’s financial puzzle. Understanding this segment is key to understanding why Microsoft is willing to pay nearly $70 billion.

The Blizzard Factor

Unlike many publishers who rely on third-party storefronts, Blizzard Entertainment operates its own platform: Battle.net. By selling World of Warcraft subscriptions and Overwatch microtransactions directly to consumers on PC, Blizzard avoids the 30% "platform tax" charged by Sony, Microsoft, and Steam. This direct-to-consumer (DTC) revenue is highly profitable and provides a level of independence rare in the industry.

The Nintendo Exclusion

Nintendo’s contribution to Activision Blizzard’s revenue is notable for what it isn’t. Because Activision is not required to declare Nintendo as a major customer (which usually happens at the 10% threshold), we know that the Switch accounts for less than a tenth of the company’s income. This suggests that Activision’s core franchises, such as Call of Duty, have yet to fully penetrate the Nintendo ecosystem—a "growth opportunity" Microsoft has frequently cited in its defense of the deal.

The King Powerhouse

In the mobile sector, King continues to be a juggernaut. While Call of Duty is the most famous brand, Candy Crush is often the more consistent earner. By bringing King under the Xbox Game Studios umbrella, Microsoft immediately becomes a top-tier player in the mobile space, a market where they previously had almost zero presence.

Official Responses and Regulatory Landscape

The acquisition has triggered a geopolitical regulatory battle, with different agencies viewing the 10% Microsoft revenue figure through different lenses.

The FTC’s Evolving Doctrine

Under the leadership of Chair Lina Khan, the FTC has moved away from the traditional "Consumer Welfare Standard," which primarily looked at whether a merger would lead to higher prices for consumers. Instead, the FTC is examining "Vertical Foreclosure"—the idea that Microsoft could use its control of Activision content to disadvantage rivals like Sony, even if prices stay the same.

The fact that Microsoft currently represents less than 10% of Activision’s revenue is being used by the FTC as evidence of how much "market disruption" Microsoft could cause if it decided to make that content exclusive or prioritized on its own platforms.

Microsoft’s Defense

Microsoft’s legal team has used these same statistics to argue the opposite. Their stance is that it would be financially "irrational" to withhold Activision content from Sony, given that Sony represents a larger portion of Activision’s revenue than Microsoft itself. They argue that the acquisition is about expansion—specifically into mobile and PC—rather than exclusion in the console market.

Sony’s Opposition

Sony Interactive Entertainment (SIE) has been the most vocal critic, telling regulators that Call of Duty is an "essential" franchise that influences console choice. Sony argues that even if Microsoft keeps the game on PlayStation, they could degrade the experience or offer exclusive "Game Pass" benefits that would inevitably tilt the market toward Xbox.

Implications: A Strategic Shift in the Gaming Hierarchy

The realization that Microsoft accounts for such a small slice of Activision’s current revenue has profound implications for the future of the industry.

1. The Dilution of the "Console War"

For decades, the industry has been defined by the rivalry between Xbox and PlayStation. However, these financial figures suggest the "Console War" is becoming a secondary theatre. The real battle is for the "Everywhere" market—mobile, cloud, and PC. Microsoft isn’t buying Activision to "win" the console war; they are buying it to transcend the console market entirely.

2. The Game Pass Multiplier

If Microsoft successfully integrates Activision Blizzard, the goal is to shift that "less than 10%" figure toward the majority. By placing titles like Diablo, Call of Duty, and World of Warcraft on Game Pass, Microsoft aims to convert Sony and Mobile customers into Xbox ecosystem subscribers. This is a move toward a "platform-as-a-service" model where the hardware (the console) becomes irrelevant.

3. Regulatory Precedents

The FTC’s stance on this deal will set the tone for the next decade of big tech acquisitions. If the deal is blocked despite Microsoft’s relatively small current share of the publisher’s revenue, it sends a signal that "potential power" is just as regulated as "current market share."

4. The Rise of Direct-to-Consumer Models

The 43% of revenue coming from non-major platforms highlights the value of owning the distribution channel. Microsoft’s interest in Blizzard’s Battle.net infrastructure suggests they want to learn how to bypass the traditional 30% fees of other platforms, potentially creating a unified Xbox/Battle.net storefront that spans PC and mobile.

Conclusion

The financial data of Activision Blizzard serves as a reality check for industry observers. It reveals a company that, while synonymous with console gaming, is actually a diversified digital powerhouse where Microsoft is currently a minor player. The $68.7 billion bid is an aggressive attempt by Microsoft to buy its way into the 90% of the market it does not currently control. Whether regulators view this as a fair expansion or a monopolistic grab will determine the shape of interactive entertainment for years to come.