The Revenue Paradox: Analyzing Activision Blizzard’s Platform Distribution Amid the Microsoft Acquisition

Executive Summary: The Surprising Minority of Microsoft in the Activision Portfolio

In the high-stakes world of video game mergers and acquisitions, few deals have commanded as much attention—or regulatory scrutiny—as Microsoft’s proposed $68.7 billion acquisition of Activision Blizzard. While the narrative surrounding the deal has largely centered on the "Console Wars" between Xbox and PlayStation, a closer look at Activision Blizzard’s internal financial reporting reveals a surprising reality: Microsoft accounts for less than 10% of the publisher’s total revenue.

According to data analyzed by industry expert Nicholas Lovell of Gamesbrief, and corroborated by Activision Blizzard’s annual reports, the revenue distribution of the world’s largest third-party publisher is far more diversified than the public discourse suggests. While Sony’s PlayStation platform commands a larger share than Microsoft’s Xbox, both are dwarfed by the combined might of mobile platforms. This disparity highlights a fundamental shift in the gaming landscape, where traditional consoles are no longer the primary engines of growth, and explains the strategic desperation driving Microsoft’s massive bid.

Chronology: From Independent Giant to Acquisition Target

To understand the current financial snapshot, one must look at the trajectory of Activision Blizzard over the last decade. The company’s evolution has been defined by three distinct eras: the rise of the blockbuster console franchise, the expansion into the PC "games-as-a-service" model, and the pivot to mobile dominance.

- 2008–2015: The Merger and Console Supremacy: Following the merger of Activision and Vivendi Games (the parent of Blizzard Entertainment), the company relied heavily on Call of Duty and World of Warcraft. During this era, retail sales on PlayStation and Xbox were the undisputed kings of the balance sheet.

- 2016: The King Acquisition: In a move that would redefine the company’s revenue streams, Activision Blizzard acquired King Digital Entertainment, the makers of Candy Crush, for $5.9 billion. This integrated a massive mobile audience into their ecosystem, providing a stable, high-margin revenue stream that offset the cyclical nature of console releases.

- January 2022: The Microsoft Announcement: Microsoft stunned the industry by announcing its intent to acquire Activision Blizzard. The deal was framed as a way for Microsoft to bolster its "Game Pass" subscription service and gain a foothold in the mobile market.

- August 2022: Financial Re-evaluation: As regulatory bodies like the Federal Trade Commission (FTC) in the U.S. and the Competition and Markets Authority (CMA) in the UK began their deep dives, analysts began dissecting the 2021 annual reports. It was here that the "less than 10%" figure for Microsoft revenue became a focal point of strategic discussion.

Supporting Data: Dissecting the 57% Platform Concentration

The financial filings from 2020 and 2021 offer a granular look at where Activision Blizzard’s billions actually come from. The company’s revenue is categorized by platform, revealing a stark hierarchy of influence.

The Big Four Platforms

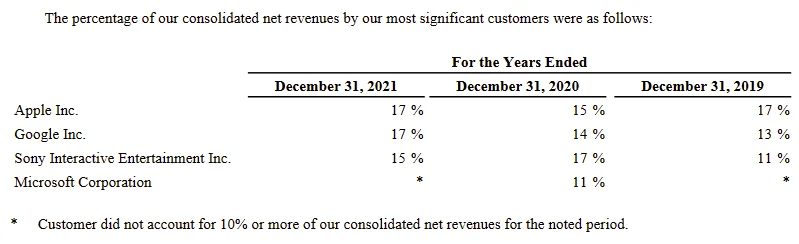

The four primary gatekeepers—Apple, Google, Sony, and Microsoft—collectively accounted for approximately 57% of Activision Blizzard’s total revenue. However, the breakdown within that 57% is telling:

- Mobile (Apple and Google): These two platforms represent approximately one-third (33%) of the company’s total revenue. This is driven almost entirely by King’s mobile titles and the massive success of Call of Duty: Mobile.

- Sony (PlayStation): Sony remains a critical partner, consistently accounting for more than 10% of revenue—often cited as being in the 15-20% range. The Call of Duty franchise’s historical marketing deals with PlayStation have solidified this lead over Xbox.

- Microsoft (Xbox): Despite being the potential acquirer, Microsoft accounted for less than 10% of Activision Blizzard’s revenue. This is a staggering statistic, as it places the "home" platform of the future parent company behind its chief rival, Sony, and well behind the mobile giants.

The "43% Elsewhere" Mystery

Perhaps the most intriguing data point is the 43% of revenue that does not come from the "Big Four." This "elsewhere" category represents a massive, decentralized portion of the business:

- Direct-to-Consumer (PC): Blizzard Entertainment’s ecosystem, centered on the Battle.net launcher, allows the company to bypass platform fees for games like World of Warcraft, Overwatch, and Hearthstone. This high-margin revenue is a cornerstone of the company’s profitability.

- Nintendo: While a major player in the hardware space, Nintendo’s share of Activision Blizzard revenue is estimated to be less than 10%, as the publisher’s most intensive titles (like Call of Duty) have historically skipped the Switch platform.

- Steam and Third-Party PC: Sales via Valve’s Steam platform and other PC storefronts.

- Territorial Partnerships: Significant revenue from China, largely facilitated through licensing deals with NetEase (prior to the 2023 hiatus), accounts for a large portion of the Asian market footprint.

- Advertising: King’s robust in-game advertising business contributes hundreds of millions of dollars annually, independent of direct consumer spending on app stores.

Official Responses and Regulatory Friction

The revelation of these revenue splits has become a tactical weapon in the ongoing legal battles surrounding the acquisition.

The Microsoft Defense

Microsoft has used these figures to argue that they are "third place" in the console market. By highlighting that they represent less than 10% of Activision’s revenue, Microsoft’s legal team has argued that the acquisition is not about monopolizing a market they already dominate, but rather about gaining the scale necessary to compete with Sony and, more importantly, Google and Apple.

The Sony Opposition

Sony Interactive Entertainment (SIE) has countered by focusing on the "must-have" nature of Call of Duty. Their argument to the FTC and the European Commission is that even if Microsoft’s current share is small, the ownership of the IP would allow them to withhold content, thereby damaging Sony’s 15-20% revenue contribution and tipping the scales of the entire industry.

The FTC’s Stance

Under the leadership of Chair Lina Khan, the FTC has signaled a move away from the traditional "consumer welfare standard," which primarily looked at whether a merger would raise prices. Instead, the FTC is looking at "vertical foreclosure"—the idea that Microsoft could use its control of Activision’s content to disadvantage rivals across multiple markets, including cloud gaming and subscription services. The fact that Microsoft currently represents a small slice of the pie is, in the FTC’s view, less important than what they could do with the 90% of the pie they are trying to buy.

Implications: Why the "Small" Microsoft Share Matters

The realization that Microsoft is a minority contributor to Activision Blizzard’s success has profound implications for the future of the gaming industry.

1. The Mobile-First Strategy

The data confirms that Microsoft is not spending $68.7 billion just to sell more Xbox consoles. The real prize is the one-third of revenue generated on mobile. Microsoft currently has almost zero presence in mobile gaming; by acquiring King and the mobile versions of Activision’s IP, they instantly become one of the largest mobile publishers in the world. This is a strategic pivot toward a platform-agnostic future.

2. The Erosion of Console Centrality

For decades, the gaming industry was defined by the hardware under the TV. These revenue figures prove that this era is ending. When 43% of a giant publisher’s revenue comes from "elsewhere" and 33% comes from mobile, the "Console War" begins to look like a regional skirmish rather than the main event. The "elsewhere" category—specifically direct-to-consumer PC gaming—offers better margins and more control, which is where the industry is heading.

3. The Power of Direct Distribution

Blizzard’s ability to generate massive revenue through Battle.net serves as a blueprint for the industry. By avoiding the 30% "platform tax" charged by Apple, Google, Sony, and Microsoft, Blizzard retains a much higher percentage of every dollar spent. Microsoft’s interest in Activision likely includes an interest in scaling this direct-to-consumer model across their entire portfolio.

4. Regulatory Precedents

If the FTC or other regulators block the deal despite Microsoft’s relatively small current share of the revenue, it will set a new precedent for "Big Tech" acquisitions. It would signal that the potential for future dominance is a valid reason for intervention, even in a fragmented market where the acquirer is currently a minority player.

Conclusion

The financial reality of Activision Blizzard challenges the common perception of the gaming market. While the public focuses on the rivalry between the Xbox and PlayStation brands, the balance sheet tells a story of mobile dominance and the power of independent PC ecosystems. For Microsoft, the acquisition is an admission that the traditional console model is insufficient for future growth. For the rest of the industry, it is a reminder that the platforms we think are "big" are often smaller than the vast, multi-platform ecosystem that today’s gamers actually inhabit. As the deal moves through its final regulatory hurdles, these numbers will remain the North Star for understanding why Microsoft is willing to pay such a historic premium for a company that currently derives 90% of its income from Microsoft’s competitors and independent channels.

Leave a Comment