The Paradox of Power: Analyzing Activision Blizzard’s Revenue Streams Amidst the Microsoft Acquisition

The landscape of the global video game industry was fundamentally altered in early 2022 when Microsoft announced its intent to acquire Activision Blizzard for a staggering $68.7 billion. While the headlines focused on the sheer scale of the deal—the largest in the history of the tech sector—a closer look at Activision Blizzard’s internal financial reporting reveals a surprising reality about the company’s revenue distribution.

Contrary to the popular narrative of a "console war" centered on Xbox, Microsoft currently represents a relatively minor portion of Activision Blizzard’s bottom line. As industry analysts, including Gamesbrief founder Nicholas Lovell, have noted, the financial data suggests that the strategic impetus for the merger lies not just in strengthening the Xbox brand, but in capturing the massive mobile and multi-platform segments where Microsoft has historically struggled to gain a foothold.

Main Facts: A Surprising Revenue Distribution

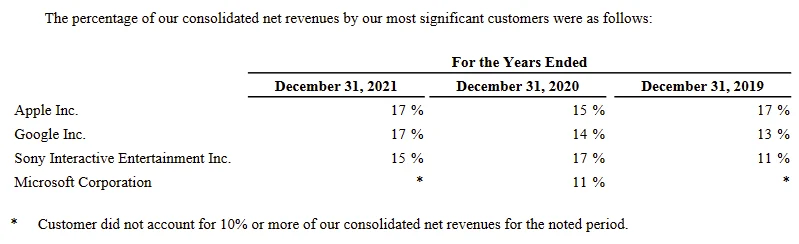

According to Activision Blizzard’s 2021-2022 annual reporting, the company’s dependence on Microsoft as a platform provider is unexpectedly low. At the time of the merger’s peak scrutiny in August 2022, Microsoft accounted for less than 10% of Activision Blizzard’s total revenue. In contrast, Sony—Microsoft’s primary rival in the console space—represented a significantly larger share of the company’s earnings.

The data highlights a tripartite division of Activision Blizzard’s financial ecosystem:

- The Mobile Dominance: Apple and Google’s mobile platforms combined to account for approximately one-third (33%) of the company’s total revenue, driven largely by the massive success of King (the makers of Candy Crush) and the mobile expansion of the Call of Duty franchise.

- The Platform Paradox: While Microsoft is the entity seeking to acquire the publisher, it currently trails behind Sony in terms of revenue generation for Activision Blizzard’s titles.

- The "Hidden" 43%: A substantial portion of the company’s income—roughly 43%—originates from sources outside the "Big Four" (Apple, Google, Sony, Microsoft). This includes Nintendo, PC platforms like Steam and Blizzard’s proprietary Battle.net, advertising revenue, and direct-to-consumer subscriptions for titles like World of Warcraft.

These figures underscore a critical shift in the industry: the traditional console market, while prestigious, is no longer the primary driver of growth for the world’s largest third-party publishers.

Chronology of the Acquisition and Regulatory Scrutiny

The journey of the Microsoft-Activision Blizzard deal has been defined by intense regulatory friction and shifting market perceptions.

- January 18, 2022: Microsoft officially announces its plan to acquire Activision Blizzard for $95.00 per share in an all-cash transaction. The move is framed as a play for the "metaverse" and mobile gaming.

- April 2022: Activision Blizzard shareholders overwhelmingly approve the sale, despite ongoing internal controversies regarding workplace culture.

- Summer 2022: Regulatory bodies, including the U.S. Federal Trade Commission (FTC), the UK’s Competition and Markets Authority (CMA), and the European Commission, begin deep-dive investigations into the merger’s impact on competition.

- August 2022: As Nicholas Lovell points out in his analysis of the annual report, the financial reality of Activision’s revenue streams begins to inform the public debate. The realization that Microsoft accounts for less than 10% of revenue suggests that the acquisition is a "catch-up" play rather than a consolidation of an existing dominant position.

- Late 2022 – Early 2023: The FTC files a lawsuit to block the deal, citing concerns that Microsoft could withhold Activision content from rival consoles to harm competition.

Supporting Data: Breaking Down the $8.8 Billion Empire

To understand why Microsoft represents such a small slice of the pie, one must look at the specific contributions of Activision Blizzard’s three main pillars: Activision Publishing, Blizzard Entertainment, and King.

The King Factor (Mobile)

King remains the "quiet giant" of the organization. In 2021, King’s revenue grew 20% year-over-year, frequently outperforming the Blizzard segment in terms of operating income. Because King’s games are almost exclusively distributed via the Apple App Store and Google Play Store, they contribute to the 33% mobile revenue share, entirely bypassing the Xbox ecosystem.

The Blizzard Legacy (PC and Direct-to-Consumer)

Blizzard Entertainment has historically been a PC-centric developer. Titles like World of Warcraft, Hearthstone, and StarCraft are primarily played on PC. Furthermore, Blizzard utilizes its own launcher, Battle.net, which allows the company to keep 100% of the revenue from digital sales and subscriptions, rather than paying a 30% "platform tax" to Microsoft or Sony. This accounts for a significant portion of the "Elsewhere" 43% mentioned in Lovell’s analysis.

The Sony/Microsoft Split

Call of Duty is the primary driver of console revenue. Historically, the franchise has had a larger player base on PlayStation due to Sony’s larger install base during the PS4 era and various marketing exclusivity deals. This explains why Sony’s revenue contribution consistently outpaced Microsoft’s leading up to the acquisition announcement.

Official Responses and Regulatory Perspectives

The disparity in revenue has become a focal point for both the companies involved and the regulators overseeing the deal.

The Microsoft Defense

Microsoft Gaming CEO Phil Spencer has repeatedly argued that the acquisition is primarily about mobile. "We’re not buying Activision Blizzard to make games exclusive to Xbox; we’re buying them to gain expertise in mobile and to expand our footprint beyond the console," Spencer stated in various press briefings. By highlighting that Microsoft currently receives less than 10% of Activision’s revenue, the company argues it is an "underdog" in the mobile and global gaming space compared to Tencent or Apple.

Sony’s Counter-Argument

Sony Interactive Entertainment CEO Jim Ryan has taken a different stance, focusing on the "must-have" nature of Call of Duty. Sony’s argument to regulators is that even if Microsoft’s current share is small, the power to make Call of Duty exclusive—or even to provide a "degraded" version on PlayStation—would give Microsoft an unfair advantage that could force consumers to switch to the Xbox ecosystem.

The FTC’s Evolving Stance

Under the leadership of Chair Lina Khan, the FTC has moved away from the traditional "consumer welfare" standard—which only looked at whether a deal would raise prices—to a broader "ecosystem" view of antitrust. The FTC’s concern is that Microsoft could use Activision’s content to dominate the emerging cloud gaming market, regardless of what the current revenue percentages show.

Implications: Strategic Shifts and the Future of Platforms

The revelation that Microsoft accounts for a single-digit percentage of Activision’s revenue has several long-term implications for the gaming industry.

1. The Necessity of the "Multi-Platform" Model

For a company of Activision’s size, platform exclusivity is financially risky. If Microsoft were to make Call of Duty an Xbox exclusive today, they would effectively be walking away from the majority of the franchise’s current console revenue (the Sony share). This suggests that for the foreseeable future, Microsoft may be incentivized to keep major franchises multi-platform simply to recoup the $68.7 billion purchase price.

2. The Shift to Mobile and PC

The data proves that the "center of gravity" in gaming has shifted. The fact that mobile platforms and "other" sources (PC/Direct) make up 76% of revenue indicates that the traditional console market is no longer the primary growth engine. Microsoft’s acquisition is a recognition that to remain relevant, a tech giant must own the content that lives on the devices in everyone’s pockets, not just the box under the TV.

3. The End of the "Small" Platform Myth

As Nicholas Lovell noted, "Sometimes, the platforms that we think are big… are not as big as we think." The narrative of the gaming industry has been dominated by the Xbox vs. PlayStation rivalry for two decades. However, the financial data suggests this rivalry is a sideshow to the much larger markets of mobile gaming and global PC distribution.

4. Regulatory Precedents

The scrutiny of this deal, informed by the complex revenue splits across mobile and console, will likely set the tone for future tech acquisitions. Regulators are learning that in the digital economy, revenue share is only one metric; data ownership, cross-platform ecosystems, and subscription models (like Xbox Game Pass) are the new frontiers of market power.

Conclusion

The Activision Blizzard annual report serves as a reality check for those viewing the gaming industry through a narrow console-centric lens. While Microsoft’s acquisition is a move of unprecedented scale, it is being executed from a position of surprisingly low current market share within Activision’s portfolio.

The strategy is clear: Microsoft is not just buying a game publisher; it is buying a diversified revenue stream that is currently dominated by its competitors. By acquiring the 90% of revenue that it does not currently control—specifically in the mobile and PC sectors—Microsoft aims to transform itself from a console manufacturer into a global media platform that transcends hardware boundaries. Whether regulators will allow this consolidation of "the other 90%" remains the most pivotal question for the future of interactive entertainment.

Leave a Comment