The Revenue Paradox: Analyzing Microsoft’s Strategic Gambit for Activision Blizzard

Executive Summary: The Hidden Financial Map of a Gaming Giant

In the high-stakes landscape of global technology acquisitions, few deals have invited as much scrutiny or speculation as Microsoft’s proposed $68.7 billion acquisition of Activision Blizzard. While much of the public discourse has centered on the "Console Wars" and the potential exclusivity of the Call of Duty franchise, a deeper dive into Activision Blizzard’s internal financial reporting reveals a surprising reality: Microsoft, the company seeking to acquire the publisher, currently accounts for less than 10% of Activision Blizzard’s total revenue.

According to data highlighted by industry analyst Nicholas Lovell of Gamesbrief, and corroborated by Activision Blizzard’s 2021 annual report, the publisher’s revenue stream is far more diversified—and less dependent on the Xbox ecosystem—than many observers realized. With Sony (PlayStation) representing a larger share of revenue than Microsoft, and mobile platforms (Apple and Google) accounting for approximately one-third of the company’s intake, the strategic impetus for the merger appears less about consolidating a current stronghold and more about capturing a market where Microsoft has historically struggled to gain a foothold.

Main Facts: Deconstructing the Revenue Streams

The revelation of Activision Blizzard’s revenue distribution provides a stark look at the power dynamics of the modern gaming industry. In the fiscal years leading up to the 2022 analysis, the financial breakdown of the company’s "Reportable Segments" painted a picture of a mobile-first, multi-platform conglomerate rather than a traditional console publisher.

The Platform Breakdown

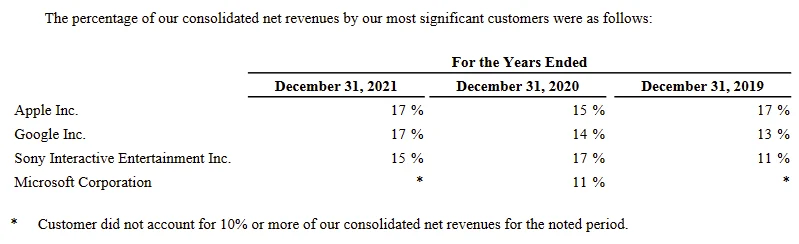

The core finding of the 2021 annual report was the relative insignificance of the Xbox platform to Activision Blizzard’s bottom line compared to its rivals. The data showed:

- Microsoft (Xbox): Contributed less than 10% of total revenue.

- Sony (PlayStation): Contributed more than 10% (historically estimated between 15% and 20% depending on the release cycle of Call of Duty).

- Mobile (Apple App Store and Google Play): Together accounted for roughly 33% (one-third) of total revenue.

- The "Big Four" Aggregation: Combined, Apple, Google, Sony, and Microsoft represented 57% of total revenue in 2020.

The "Missing" 43%

Perhaps the most intriguing aspect of the data is the 43% of revenue derived from "other" sources. This category includes:

- Direct-to-Consumer PC Sales: Blizzard’s proprietary Battle.net platform, which hosts massive titles like World of Warcraft, Overwatch, and Hearthstone, allows the company to bypass platform fees associated with Steam or Epic Games Store.

- Nintendo: While a major player, Nintendo’s contribution remained under the 10% threshold required for individual disclosure in SEC filings.

- Advertising: A massive growth engine for King (the makers of Candy Crush).

- Regional Partnerships: Revenue from large territories like China, where the company operated through local partners such as NetEase.

Chronology: The Road to the $68.7 Billion Deal

To understand the strategic importance of these numbers, one must look at the timeline of the acquisition and the shifting priorities of the parties involved.

- February 2016: Activision Blizzard completes its acquisition of King Digital Entertainment for $5.9 billion. This marks the beginning of the "mobile-first" shift, which eventually led to mobile becoming the company’s largest revenue segment.

- January 18, 2022: Microsoft announces its intent to acquire Activision Blizzard for $95.00 per share in an all-cash transaction. The deal is positioned as a move to accelerate Microsoft’s growth in mobile, PC, console, and cloud gaming.

- April 2022: Activision Blizzard stockholders overwhelmingly approve the merger, with over 98% of shares voted in favor of the transaction.

- August 2022: Financial analysts begin dissecting the 2021 annual reports as the Federal Trade Commission (FTC) and international regulators (such as the UK’s CMA) ramp up their investigations. Nicholas Lovell’s analysis highlights the irony of Microsoft’s small revenue share in its target acquisition.

- Late 2022: The FTC, under the leadership of Chair Lina Khan, signals a more aggressive stance toward the merger, moving beyond traditional consumer price harm to look at broader ecosystem competition.

Supporting Data: The Ascendance of Mobile and the "King" Factor

The data underscores a fundamental shift in the gaming industry: the decline of console dominance. For decades, the industry was defined by the hardware cycles of Nintendo, Sega, Sony, and later Microsoft. However, Activision Blizzard’s financials prove that the "Console War" is now a secondary theater of operations.

The King of Mobile

The inclusion of King in the Activision Blizzard portfolio fundamentally altered the company’s financial DNA. In many quarters, King’s operating income has rivaled or exceeded that of the Activision (Call of Duty) and Blizzard (Warcraft) segments. Because mobile gaming relies on microtransactions and high-frequency engagement rather than one-time $70 hardware-locked purchases, it provides a more stable, recurring revenue stream.

The Direct-to-Consumer Edge

Blizzard Entertainment’s reliance on Battle.net is a critical component of the "Other" 43% revenue bracket. By maintaining its own launcher and ecosystem on PC, Blizzard avoids the 30% "platform tax" charged by Valve (Steam) or Microsoft (Windows Store). This vertical integration makes Blizzard’s PC revenue significantly more profitable per dollar than its console revenue.

Strategic Parity

The fact that Microsoft accounts for less than 10% of revenue suggests that Activision Blizzard was, in many ways, "platform agnostic." This independence gave them significant leverage in negotiations. For Microsoft, buying the company is not just about gaining content; it is about capturing the 90%+ of revenue that currently flows to Apple, Google, Sony, and internal PC systems.

Official Responses and Regulatory Context

The disparity between Sony’s and Microsoft’s revenue shares from Activision titles has become a central pillar of the legal battles surrounding the merger.

The Sony Objection

Sony Interactive Entertainment (SIE) CEO Jim Ryan has been a vocal critic of the deal, arguing that Microsoft could eventually make Call of Duty exclusive to Xbox. Sony’s concern is rooted in the very data Lovell highlighted: because Sony represents a larger portion of Activision’s revenue than Microsoft, the loss of those titles would be a devastating blow to PlayStation’s ecosystem and its "Store" commission revenue.

Microsoft’s Defense

Microsoft Gaming CEO Phil Spencer has countered these concerns by arguing that it makes no financial sense to "pull" Call of Duty from PlayStation. Given that Microsoft currently receives less than 10% of the revenue, cutting off the Sony revenue stream (which is larger) would make the $68.7 billion price tag impossible to recoup. Microsoft has offered 10-year "parity" deals to Sony, Nintendo, and Steam to appease regulators.

The FTC’s New Stance

Under Chair Lina Khan, the FTC has adopted a "wider definition of anti-trust harm." Traditional antitrust law focused on whether a merger would lead to higher prices for consumers. Khan’s FTC, however, looks at "vertical foreclosure"—the idea that a company could use its control over a key input (like Call of Duty) to disadvantage rivals in adjacent markets, such as cloud gaming or subscription services (Game Pass).

Implications: Why the "Small" Microsoft Share Matters

The realization that Microsoft represents a minority of Activision Blizzard’s revenue has several long-term implications for the gaming industry and the future of digital platforms.

1. The Pivot to Mobile and Cloud

Microsoft’s primary motivation is clearly not console hardware sales. By acquiring Activision Blizzard, Microsoft instantly becomes a major player in mobile (via King) and gains a massive library for its Game Pass subscription service. The goal is to move toward a "device-agnostic" future where the 33% of revenue currently going to Apple and Google can be funneled through Microsoft’s own cloud infrastructure.

2. The End of the Traditional Console War

If the deal closes, the "Big Four" platforms will be consolidated into a "Big Three" (Apple, Google, and Microsoft/Sony). However, with Microsoft owning the content that generates the most revenue on Sony’s platform, the traditional rivalry changes. Microsoft becomes Sony’s most important third-party publisher, creating a strange "frenemy" dynamic where Microsoft profits every time a PlayStation owner buys a digital skin in Warzone.

3. Regulatory Precedents

The FTC’s scrutiny of this deal, despite Microsoft’s low current revenue share of the target company, suggests a new era of regulation. Regulators are no longer looking at what a company is today, but what it could become if it controls the most popular intellectual properties in the world.

4. The Hidden Strength of "Other"

The 43% of revenue from non-major platforms highlights the importance of the PC market and direct-to-consumer relationships. For developers, the lesson is clear: while the major platforms (Sony, Microsoft, Apple, Google) are essential, the most sustainable long-term strategy involves building a direct relationship with the audience, as Blizzard did with Battle.net.

Conclusion: A Strategic Re-Alignment

Nicholas Lovell’s observation serves as a necessary reality check for an industry often blinded by "console-centric" thinking. The fact that Microsoft accounts for less than 10% of Activision Blizzard’s revenue is not a sign of weakness, but rather the very reason the acquisition is so vital for Microsoft’s future. To compete with the mobile dominance of Apple and Google and the hardware install base of Sony, Microsoft isn’t just buying a game studio—it is buying a massive, diversified revenue engine that has already mastered the platforms where Microsoft is currently a minor player.

As the regulatory dust settles, the industry will likely look back at these charts as the blueprint for Microsoft’s transformation from a software and console company into a global gaming utility.

Leave a Comment